We receive questions from time to time on why our Forex testing tools only support one month of data. These questions obviously arise because Smart Forex Tester and Simulator GUI has a tab with one month calendar.

As a matter of fact, both Tester and Simulator can work with unlimited data.

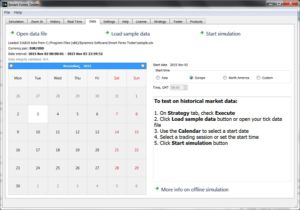

A monthly calendar view was added to provide an easy way to select when to start the test (stopping the test can be obviously done any time).

But on this occasion, it would be good to discuss here whether we really need big data files in Forex testing.

The only argument in favor that we can imagine is the need to test strategies that use long time frames.

But if we really wanted to use such strategy, does it make sense? Do we have enough time for that? And even if we do, we need to have a lot of money invested to satisfy margin requirements. Unless you trade with large sums without any leverage.

And even more questionable are the benefits of testing on the long intervals for the most commonly used optimization methods, when a given set of strategy parameters are permutated to make the strategy work best on the historical data.

Unfortunately, it doesn’t guarantee the strategy will win when used the very next day – whatever long interval you tested it on. This is the reason we use a principally different approach.

We are developing the mechanism to adjust the strategies to the current market automatically on the fly. So, we test our automated trading strategies on 1 week long test data.

There are several reasons behind this testing interval selection. The primary one is continuity in the price quotes. If you leave a position open over weekend, you always risk hitting a price gap. If something happens during the weekend, the gap can easily be several hundred pips. And stops sometimes can not be even triggered.

Next, it takes reasonably short time to run a test on one week of quotes. is not too long to run.

Of course, big price moves can happen during the trading week, as well. However, it’s not a gap – but a very fast moving market. So you might be able to do something yourself and stops might work.

In addition, quite often such turbulence is news related and so can be predicted, as the major news releases are mostly scheduled.

Our approach is to use one week as a standard interval that is easy and quick to run and analyze. Based on the analysis, we select certain data intervals that are worth using later. Mainly, those where the strategies loses systematically.

Only these intervals are worth testing on. Markets quite often just treading water. Testing on such data is just wasting time.

So we prefer to collect a set of test cases that represent the market conditions that are difficult for the strategies to handle. Running the set is an efficient “smoke test” – if the strategy is failing, there is no need to go deeper and run longer tests.

Based on weekly test results, we can select most important parts of the data and us them later as test scenarios. They can be as short as one trading session. Often the market behavior is the same during one session, but the next session might not continue the pattern.

Best is to test overlapping new York and London sessions when the moves are most powerful.

You can use our free Forex Data Manager to slice a month long .csv data files into one week (or smaller) ones.